Introduction

Welcome to our Trade Lane Review, a special publication to satisfy the demand for more insight on the outset of 2025’s new alliance structures. We will primarily focus on the major E/W trades leading into this transitional period: Far East - West Coast North America, Far East - East Coast North America, and Far East - Europe.

With no shortage of catalysts at play like tightened tariffs under the new Trump administration, Lunar New Year blank sailings, and schedule reliability recovery from 2024’s rail shortages and strikes, we’re definitely in for a productive and somewhat chaotic Q1. This is of course made all the more dynamic by Premier Alliance and Gemini Cooperation taking center stage. In this report we provide a trade capacity overview of the Far East - West Coast North America trade as well as detailed examples of some interesting service schedule restructures and delays. You are welcome to reach out to our team directly with questions, comments, or requests for deeper insight and access to eeSea’s wealth of container shipping data. Please see our Contact and Methodology sections below for details.

Key takeaways

- We can expect to see a slump in planned capacity in the month of February but there is no indication that network transitions will cause a notable decline in actual delivered capacity in the following months.

- Forecasted capacity faces some difficulties in accurately representing sailings lost to delays until the virgin services mature over the next few weeks.

- MSC will independently soldier on in its West Coast presence despite a lack of alliance partnership and others like WHL will join larger alliance services for the very first time.

- Despite best laid plans, many services are already experiencing struggles with vessel delays, albeit significantly scaled back from their predecessors. Ad-hoc measures like delayed start dates, strategic blanks, and port omissions are employed.

- Some new services share little more than a name with their former iterations while others maintain a fairly close resemblance to the old and reveal possible reliability improvements through some clever structural tweaks.

Trade capacity stabilization during transitions

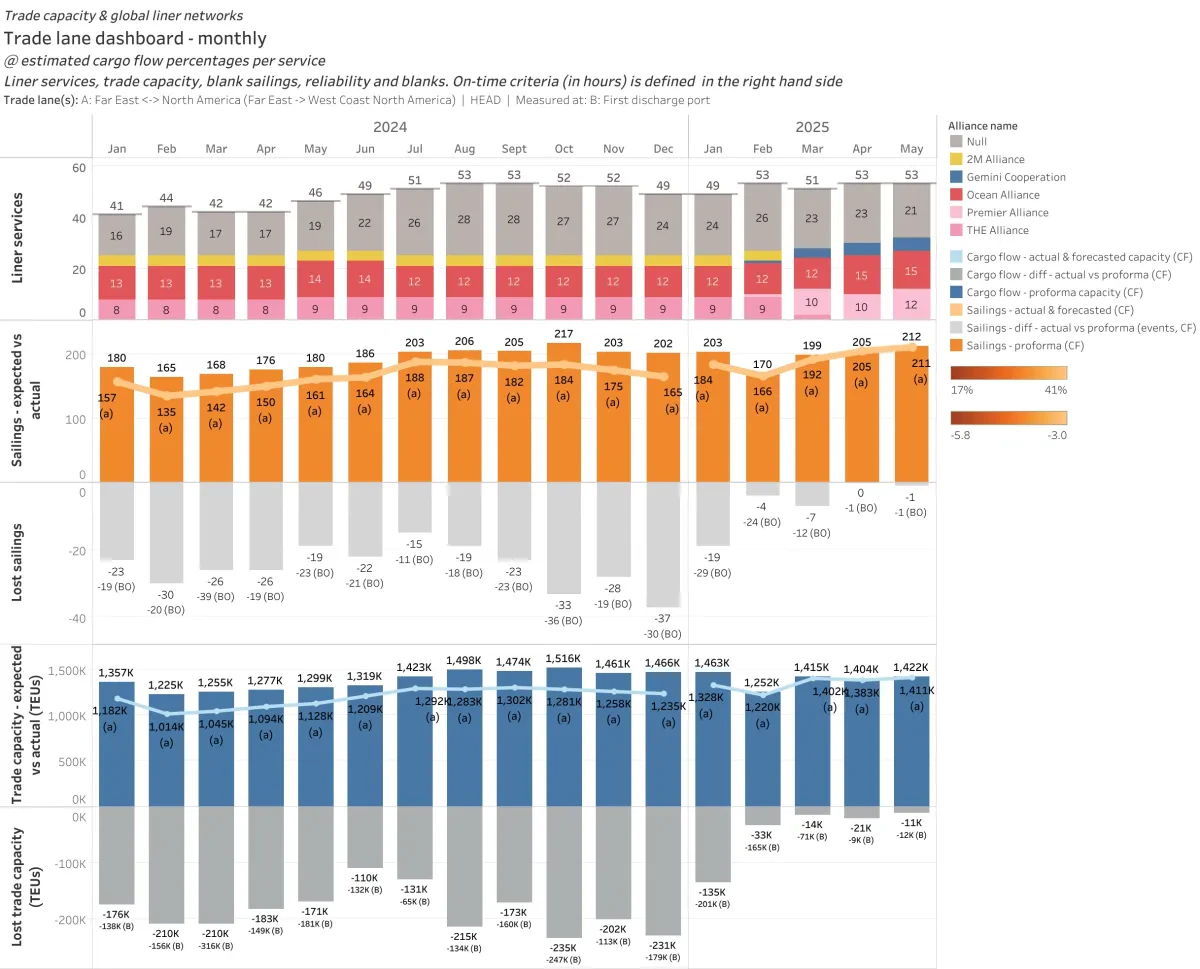

The Far East - West Coast North America trade currently hosts 49 services in January 2025, 2 of which are part of the more complex pendulum service category: MSC - Swan-Sentosa and THEA - PS3. There are 12 OCEAN Alliance services, 9 by THE Alliance, 4 by 2M Alliance, and 24 non-alliance services. The Premier Alliance and Gemini Cooperation will introduce 10 and 5 new services, respectively.

Looking back, January 2024 started out with 42 services and peaked at a total of 53 in Q3 and Q4 before coming back to 49 at the close of the year. Due to the expected overlap of old vs. new services in transition, February 2025 reveals a spike of 62 total unique services. However, a spike in total service versions should not mislead anyone to think there will be an equal spike in capacity.

Capacity in February is forecasted to decrease due to a combination of factors: heavily delayed arrivals on service versions on their way out, blank sailings announced for the 2025 Lunar New Year, the shorter number of days this month, and gaps caused by some alliance services petering out as early as December whilst others have had their start dates pushed back by a week, or even months, in cases like PMR - PN4. The first two factors primarily impact actual (aka forecasted) deployed capacity while the shorter days of the month and gaps in service suspension vs. service introduction impact expected (aka proforma) capacity.

In a rarer occurrence, the Lunar New Year uniquely impacts both proforma and forecasted capacity when paired with the timing of these new alliances. Carriers would normally be using standardized blank sailings to account for the Chinese holiday capacity loss during this period, but the fact that it closely coincides with the suspension of many services means they can simply schedule the final voyages for services like THEA - PS3 as early as week 5. With the new PMR - PS3 not set to commence first sailings until week 7, this creates a natural lull in expected proforma events.

Trade lane overview - monthly

January has so far seen an actual 1,328K TEU of its expected 1,463K capacity. February is forecasted to see 1,220K TEU’s of actual capacity arriving into West Coast gateways opposed to a proforma capacity of 1,242K TEU. Usually, the monthly difference from lost sailings on the West Coast is more significant than 32K, but the arrival of new services means many existing delays are being ‘reset’ by virgin proforma schedules. This pattern in expected vs. forecasted capacity is also observable in the following months through May. The differences will become more pronounced as the new services begin to accrue delays that are organically built into eeSea’s live vessel forecasts.

The heavy slump in proforma capacity for February becomes less daunting if we dive down into a weekly view. The largest dips in planned proforma events occur in weeks 7 through 9, with ~7% of the lost events being explained by the shorter 28 day duration of this month and the rest being accounted for by gaps in service hand-offs like the PS3 explained above. The capacity slump normalizes back to pre-transition values in the ~330K TEU range by the time we reach week 13 at the end of March. Similarly, while the monthly view shows a dramatic spike to 62 services in February, the weekly dashboard more aptly illustrates that there will not be more than 48 unique services active on any given week.

Trade lane overview - weekly

Trade capacity evolution by alliance

Here we look at the average expected capacity (prorated by cargo flow) and weekly sailings into first ports of discharge by alliance. We have defined the lead up period as October 28, 2024 - March 2, 2025 and the post-transition period as March 3 - May 4, 2025; a total of 27 weeks/6 months. Note that there are service outliers from both old and new alliances that overlap in weeks 9 and 10. We expect that any average values in Gemini Cooperation and Premier Alliance sailings brought down by the first choppy weeks in February and March will be better balanced from May onward.

- OCEAN Alliance - 12 sailings/wk @108K TEUs total vs. 13 sailings/wk @ 110K TEUs total

- 2M Alliance - 4 sailings/wk @39K TEUs total vs. full suspension

- THE Alliance - 8 sailings/wk @69K TEUs total vs. full suspension

- Gemini Cooperation - non-existent vs. 4 sailings/wk @38K TEUs total

- Premier Alliance - non-existent vs. 10 sailings/wk @79K TEUs total

- Non-Alliance - 21 sailings/wk @108K TEUs total vs.19 sailings/wk @94K TEUs total

Trade capacity index for transitioning alliances - monthly

While Maersk Line will be maintaining a familiar cadence in the number of sailings and average weekly capacity in its new partnership, Hapag Lloyd’s participation in weekly sailings on the Transpacific are halved along with a 45% decrease in alliance capacity. In addition to their carefully plotted hub-and-spoke web of shuttles, Gemini Cooperation’s conservative number of sailings may be an indicator into how they plan to deliver improved reliability on the West Coast North America trade.

Conversely, former members of The Alliance - HMM, ONE, YML - will increase their weekly sailings from 8 to 10 and see an additional 15% in deliverable capacity. Premier Alliance partners will notably be joined by Wan Hai Lines on the PMR - PS6 and PMR - PS7. This opportunity is huge for WHL which is primarily active in Asian intra-regional and feeder trades. They currently participate in just 2 non-alliance service offerings for the Far East - North America trade, and 9 in the Far East - Middle East. Their only West Coast North America offering is the WHL - AP1 where they are partnered with HMM and ONE.

Please note that Ocean Alliance’s Day 9 Product is still under active investigation and undergoing regular updates. While our team has already implemented high level rotation changes communicated in their advisory from January 13, details regarding actual vessel voyages remain non-definitive at this time.

MSC remains resilient without alliance support

Much like ONE’s non-alliance collaboration with Ocean Alliance partners on the Transatlantic trade, MSC’s cameos on Premier Alliance routes will be concentrated on the Far East - Europe trade. The PMR - FP2 and the PMR - FE6 are two exceptional pendulum category alliance services calling the West Coast where MSC is will participate. The FP2 is a unique continuation of the former West Coast service, THEA - PN2 and is an unlikely early candidate for testing Suez Canal passage based on MSC's most recent commentary. On the FE6, MSC has adopted the Swan-Sentosa name from its standalone pendulum service and will continue making regular calls to Long Beach and Oakland.

With the dissolution of the 2M Alliance, they will be introducing 9 non-alliance services across both the East and West coasts. The names have been adopted from former 2M services but in many cases there are notable differences from the former rotations. The revised Mustang, Orient, and Pearl will be joining the long-standing Chinook in services bound for the West Coast gateway ports in Q1.

On the East Coast, MSC will be partnering with ZIM while maintaining dominance in VSA-based capacity as the vessel provider in all but one service, the MSC - Amberjack. The Amberjack is not classified as part of the Far East - West Coast North America trade but it is technically a Transpacific service that calls Manzanillo (MX) before heading to the Panama Canal, Kingston, and then Savannah, Charleston, and Wilmington (NC) before looping back through Panama to Busan.

With the total number of their direct Far East - West Coast services fully halved from 8 to 4 (not including Premier pendulums), MSC will see a 43% drop in proforma capacity from 63K to 36K weekly TEUs with its new non-alliance services. If we include the weekly capacity expected to arrive into the first discharge ports of Long Beach and Vancouver on the FE6 and FP2, that’s an additional 20K TEUs per week, bringing the total to 56K and a less grim total 10% capacity decrease.

Trade capacity index for MSC - monthly

Service examples: schedule outliers

Far East - West Coast North America was arguably the first of the E/W trades to have the most comprehensively detailed schedules available during the past few months of initial discovery, specifically P2P schedules and vessel assignments. Even as we approach the global commencement dates for many new services next week, it still shows more general stability than the Far East - East Coast North America and Far East - Europe trades. That said, there are still lingering doubts and a few outliers. Here is a non-exhaustive list of some exceptional services.

Premier Alliance

- PMR - PS5 is postponed until May for the time being and no participating partners are showing any voyage details as of yet.

- PMR - PN3 proforma schedules for the first sailings were pushed back by a full week as recently as the last 48 hrs in order to counteract delays on THEA - PN3’s final sailings and ensure a clean slate for the new service. See details below.

- PMR - PN4 had her original start dates scaled all the way back to 01-05-2024, possibly due to the weather related difficulties expected in Vancouver during Q1 and heavy delays from its predecessor.

- PMR - PS3 began earlier than its fellows with the CONTI CONQUEST starting her first sailing on 23-01-2025 but is already facing delays. See our special analysis of this service for more details.

Gemini Cooperation

- GEM - WC5 is slated to have a bit of a late start compared to its peers and was also slow to reveal voyage details. The HUDSON EXPRESS will be the first sailing bound for Los Angeles with ETA April 08-04-2025. Slot 2 is still TBD but the COLORADO EXPRESS will join Slot 3 on 30-03-2025.

- GEM - US2 uniquely calls both North American coasts via New York, Norfolk, and Los Angeles and saw its start date advanced by a week from 17-02-2025 to 10-02-2025 within the past 14 days.

Service examples: rotation comparisons

One question our team has received persistently is for details on how the ‘old’ differs from the ‘new’ on a service level. The issue is far from black and white: many new alliance services are most consistent in maintaining namesakes, trade, and of course expected VSA participation. However, when we get down to the granular details of number of calls, port rotation, and even average vessel size, the differences between the two can be significant. We hesitate to label any of these transitive services as completely ‘mirroring’ one another even in the clearest examples.

Here is a non-exhaustive list where we present instances of both scenarios: a ‘repackaging’ in name alone vs. a fairly close rendition of a service from its predecessor. In regards to the Gemini Cooperation examples below; while the alliance-level names themselves have not been carried over, we have highlighted the ones where Maersk Line has retained namesakes from its 2M partnership with MSC.

Premier Alliance

- THEA - PN3’s final v16, active since 19-04-2024, was a 63 day roundtrip with a total of 9 calls. The PMR - PN3 will have a 49 day roundtrip with just 7 calls. Avg. vessel capacity will be dropping from 11.8K TEU to 5.4K TEU. The WC ports remain the same with Vancouver still preceding Tacoma. Hai Phong, Yantian, and Kaohsiung have been dropped and replaced by Qingdao and Ningbo.

- THEA - PS3 v18 and the first iteration of the PMR - PS3 port rotation remain identical with WC ports Los Angeles and Oakland taking center stage. The PS3 will be increasing her roundtrip to 84 days and adding an additional slot for 12 vessels. Average vessel sizes remain relatively unchanged.

- THEA - PN4 which has suffered some of the more infamous delays discussed amongst stakeholders on the West Coast Gateway since Q2 2024, is undergoing quite the overhaul with its transition into PMR - PN4. The service will drop from 9 to 4 calls while maintaining a roundtrip of 42 days and increasing vessel sizes from the 7K TEU to 10K TEU range. Qingdao is dropped along with Busan, Kwangyang, and Prince Rupert and Vancouver is shifted into the first discharge port position ahead of Tacoma.

- THEA - PS6 will suspend and continue only in name in the form of the PMR - PS6. Throwing us for a real loop in the name vs. rotation game, the PMR - PS6 is actually a near match for the soon to be suspended non-alliance service, the HL - PSX. The primary differences here between the new PS6 and the old PSX will be an increase of roundtrip time from 49 to 56 days, the addition of 2 new calls at Qingdao and Ningbo, and an increase to 8 slots. Other than this the port rotation is an exact carry-over as well as the entire vessel lineup for the first round of deployments.

Gemini Cooperation

- GEM - WC1 is a fairly comparable carryover from 2M - WCNA loop 2 v10 with Maersk Line reusing the TP6 name. WC1 will see a continuation of the 56 day roundtrip but a reduction to 4 calls, while retaining Los Angeles as the singular port of call on the West Coast. Xiamen, Hong Kong, and Yokohama calls are dropped as Cai Mep and Nansha are added. Vessel lineup is a direct transfer, including the first two sailings of MAERSK ANTARES and GEORG MAERSK.

- GEM - WC3, aka ML - TP1, and formerly 2M - WCNA loop 5 is facing heavy delays and still displays some uncertainty in vessel schedules, including TBN’s. The number of calls is reduced from 10 to 6, as is the roundtrip from 56 to 42 days. Ningbo and the first discharge calls for Yokohama and Busan are reduced to one call each as last load ports on the new TP1 rotation. Vessel size remains in the 7K-8K TEU range.

- GEM - US2 carries the namesake of the ML - TP12 over from pendulum service 2M - ECNA RTW pendulum but sees significant changes. There is a full week reduction in roundtrip from 91 to 84 days, 10 calls instead of 12, and a reduction of slots down to 12. Most notably, the service will no longer utilize the Cape of Good Hope but loop back through the Panama Canal, becoming an Eastbound and then Westbound journey. It will also utilize both ports on both North American coasts, dropping Baltimore but tacking on a last load call to Los Angeles on its return to Asia. While the vessel lineup looks significantly different at this time the range in sizes is fairly close between 9K-10K TEU averages.

2M - WCNA loop 5 vs. GEM - WC3 import rotation into Prince Rupert, CA

THEA - PN4 vs. PMR - PN4 import rotation into Vancouver, CA

Methodology notes

- Proforma events are planned calls that are based on service rotations provided by carrier fliers and long-term schedules. They are unique to each service version and measured as expected capacity.

- Actual events are calls that have already occurred and are reflected in our actual deployed capacity measurements. Some actual events do not have planned proforma schedules and are defined as inducements. Before an actual event has passed, it is classified as a forecasted event - distinct from proforma or expected capacity.

- Trade capacity and planned events on all counts in the analysis above were measured by the first port of discharge.

- When measuring trade capacity by trade, service, or alliance we prorate the values based on assumptions like 90% capacity being utilized at the last load port of the first leg of the journey. We also use this method to split the expected capacity for complex cargo flow services that call multiple regions in addition to the West Coast (ie Central America, East Coast North America).

- A last load port is the last call on the head haul of a cargo flow: on West Coast North America service rotations this will be defined by the final Asian port of call before the vessel sets out across the Pacific to North America. The first discharge port on the head haul is defined as the first port of call in the next leg of this cargo flow: that would be the first vessel’s first planned call in Canada or the United States.

Contact us: Please reach out to ops@eesea.com if you are an existing customer that would like to explore these stories in depth, contact@eesea.com if you are interested in collaborating on press releases or other third party publications, and commercial@eesea.com if you are a new user looking to test a use case and learn about what our data solutions can offer.

eeSea Signals

- Vancouver Inbound/Outbound Calendar

- Prince Rupert Inbound/Outbound Calendar

- Los Angeles Inbound/Outbound Calendar

- Long Beach Inbound/Outbound Calendar

- Oakland Inbound/Outbound Calendar

- Seattle Inbound/Outbound Calendar

- Tacoma Inbound/Outbound Calendar

- All Current + Upcoming Premier Alliance Services

- All Current + Upcoming Asia - North America Gemini Cooperation Services

- All Current + Upcoming Ocean Alliance Services

- eeSea TrueTransit Global Port Connectivity + Reliability Benchmarking for Far East - West Coast North America Trade

- Trade Lane Dashboard Including Schedule Reliability and Actual vs. Expected Capacity Timeline - Tableau Permission Required

- Port Calendar Including Vessel Forecasts + Delays by Service - Tableau Permission Required

- Trade Capacity Index Changes by Service + Port - Tableau Permission Required

- VSA Shares by Trade + Service - Tableau Permission Required

- Alliance Reshuffle Weekly Capacity Changes by Alliance - Tableau Permission Required