Introduction

Welcome back to part two of our Far East - North America Trade Lane Review, where we invite you to explore the interplay between old and new alliances and how this uniquely transitionary period will shape the seascape of 2025.

While we do revisit key concepts in our trade capacity overview below, the initial West Coast centric report contains a bit more detail in the explanation of measurements like proforma vs. actual & forecasted capacity. A short reference to terminology is also provided in the Methodology section at the end of this report but we highly recommend reading part one, published earlier this week on February 03, 2025.

Key takeaways

-

The proforma capacity slump illustrated in the Trade Lane Overview shifts back a little through the month of March along East Coast services, due to longer roundtrip times.

-

MSC’s presence continues to build strength along the East Coast, where it will partner exclusively with ZIM and nearly rivals its standalone West Coast offerings.

-

The prevalence of pendulum and RTW services involved in alliance transitions make for interesting case studies as we continue our examination of namesake vs. service structure carryover.

-

While there is still a need for measures like strategic blanks and pushed commencement dates, vessels are exhibiting more reduced delays in their first sailings compared to the first West Coast voyages.

Services overview

As of week 6, there are 21 total services calling the East Coast that are part of the Far East - North America trade. Of these, 8 are allotted to OCEAN Alliance, 6 to 2M, 4 to The Alliance, and another 4 to non-alliance services.

While most East Coast services travel through the Panama Canal there are one or two special outliers like the 2M’s ECNA Cape pendulum and ECNA RTW pendulum routes, or OCEAN’s PSW3 & AWE3 combo that utilizes the Cape of Good Hope on both Westbound and Eastbound loops. Another two RTW services include non-alliance examples like Hapag Lloyd’s AA7 service where they partner with WHL or BAHRI’s MEANAMRORO that calls just once every 30 days.

In the post transition period from week 15 onwards where we can more or less expect stabilization of suspensions and commencements, we will see Gemini Cooperation hosting 4 services, Premier Alliance equally providing 4, non-alliance services up to 8, and 8 again for Ocean.

While THEA’s transition to Premier Alliance will host the same number of services, the 2M dissolution sees Gemini Cooperation providing 4 and MSC’s partnership with ZIM representing 6 in the non-alliance category - a total of 14 re-envisioned services along the East Coast. We’ll take a look at whether or not these new ventures will be injecting capacity along the trade below.

Trade capacity stabilization during transitions

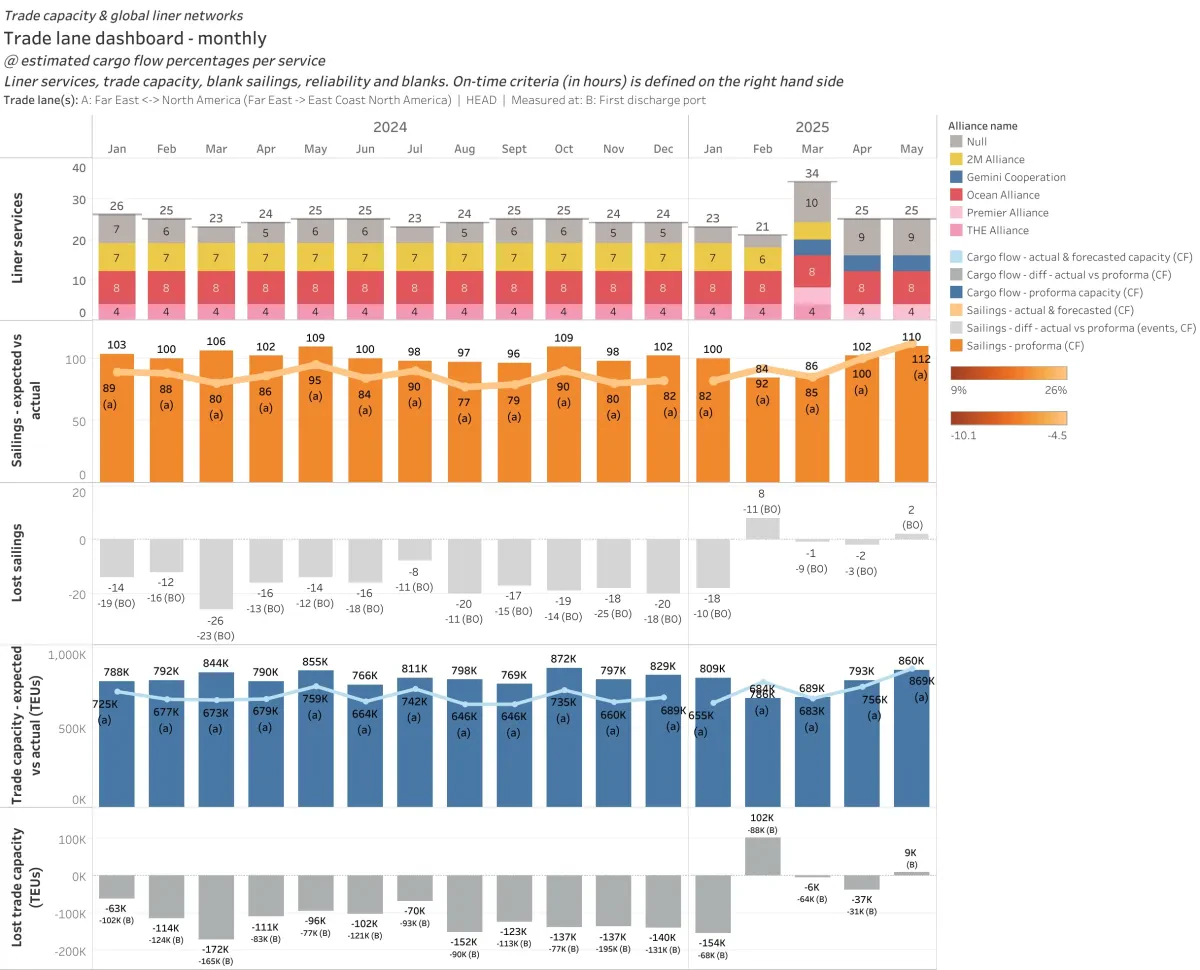

The monthly capacity overview on the East Coast reveals an unsurprising slump in Q1 and a significant peak in total unique service versions, with 35 expected to be seen throughout the course of the hand-over in March. We must reiterate that the lack of proforma capacity does not connote a lull in actual or forecasted capacity, and is actually aided by the reality of delayed arrivals from services that are being suspended. For an in depth look at how the capacity waterfall is affected by delayed arrivals, please see our previous publication.

In January we witnessed 655K TEU of actual capacity against the planned 810K - an unalarming difference of 155K in lost sailings if we look at the trend in the past 6 months. February is currently forecasted to see 685K TEU of actual capacity against 774K TEU of planned sailings, a bit more of an optimistic difference that will be tempered by accrued delay on some first sailings as the month wears on. March sees a further decrease in planned capacity down to 689K vs. 695K TEU of forecasted sailings, again likely to decrease as vessels build up delay along their new routes. April and May see planned capacity stabilizing at 803K and 859K TEU’s respectively.

One notable difference from the West Coast report is that we see the lowest planned capacity and most new service version introductions happening in the month of March instead of February. This is largely due to the longer roundtrip times for East Coast services necessitated by routing through the Panama Canal, and in some rarer cases, RTW services like the GEM - US1 that will travel around the Cape of Good Hope.

Trade lane overview - monthly

Once again, a weekly breakdown gives us a comprehensive visual representation of the capacity see-saw as these services transition. The drop in planned capacity is most pronounced in weeks 10, 11, and 12. Week 11 is the most drastic cut, due to a nearly complete lull in proforma sailings for both THEA to PMR and 2M to GEM handovers. To elaborate: in week 11 there are no scheduled sailings for either Premier Alliance or Gemini Cooperation, 2M schedules are fully suspended, and there is just a single sailing on The Alliance’s EC1. The turnover period for THEA to PMR transitions lasts for a total of 4 weeks from week 10 through 14, all the way through the end of March, while 2M to GEM see a shorter transition from week 11 through 12. Finally, despite the monthly view’s implication of 35 service versions in tandem, there really won’t be more than 25 at any given time in the months ahead.

Trade lane overview - weekly

Trade capacity evolution by alliance

A direct comparison between average expected weekly capacity (prorated by cargo flow) and total weekly sailings into first ports of discharge by alliance. The lead up period is defined as October 28, 2024 - March 2, 2025 and the post-transition period as March 3 - May 4, 2025; a total of 27 weeks/6 months.

- OCEAN Alliance - 8 sailings/wk @77K TEUs total vs. 8 sailings/wk @ 76K TEUs total

- 2M Alliance - 7 sailings/wk @47K TEUs total vs. full suspension

- THE Alliance - 4 sailings/wk @37K TEUs total vs. full suspension

- Gemini Cooperation - non-existent vs. 4 sailings/wk @20K TEUs total

- Premier Alliance - non-existent vs. 4 sailings/wk @22K TEUs total

- Non-Alliance - 4 sailings/wk @21K TEUs total vs. 8 sailings/wk @47K TEUs total

Gemini Cooperation’s representation on the East Coast is approximately half of their West Coast offering, with 20K vs. 38K TEU’s. Similarly, Premier Alliance will host 22K as opposed to 79K along the West Coast. Members of both alliances will also see an overall dip in proforma capacity from their East Coast handovers. Maersk Line’s new partnership will see a 57% drop in alliance-level capacity offerings, and Premier partners ONE, HMM, and YML will see a 41% drop. Former THEA participant Hapag Lloyd will see a drop of 46% in their old vs. new alliance capacity.

Trade capacity index for transitioning alliances - monthly

MSC & ZIM dominate non-alliance offerings

In contrast to the 3 three new services calling into West Coast North America, MSC has a broader wealth of new offerings along the East Coast, where it will also partner with ZIM on all 6 of its new services. The MSC - Amberjack is the only service where ZIM owns the majority VSA share and MSC acts as a slot charter, with MSC acting as primary vessel provider on the America, Empire, and the Lone Star Express. Both VSA partners will hold an equal share of vessel ownership on the Pelican and RTW Emerald services.

Prior to the transition, MSC’s only standalone East Coast service was MSC - Liberty, with the first port of discharge Miami. This service already suspended last month with the final sailing of the MSC CHARLESTON having departed New York City on January 9. ZIM’s only standalone East Coast offering is the RTW service, the ZIM - ZXB, which will be suspending April 25 with the final sailing ZIM ARIES being sandwiched between two blank sailings in slot 10 and 12. ZIM ARIES will make its final call into Boston on March 26.

In terms of capacity, MSC and ZIM will host 33K TEUs of weekly capacity, a 30% reduction. That said, they will still retain significantly more of planned capacity than Maersk Line with the dissolution of their former alliance. Not including their participation on Premier Alliance’s FP2 and FE6 pendulum services, MSC’s non-alliance West Coast presence will average out at 36K TEUs, roughly equalizing the carrier’s capacity offering across both coasts.

Service examples: schedule outliers

As discussed in part one of our Far East - North America trade overview, the concept of a ‘virgin’ service is often more true in theory than in practice. Many of the new alliance services will kick-off with some inherited delays from their predecessors. However, compared to the West Coast services in our previous report, East Coast services do currently show more schedule stability in their first handful of sailings.

While there are still measures like strategic blanks and delayed proforma start dates used to manage first voyages’ reliability, there has been more general success in scaling back the starting delay of these vessels to -3 days or less at the beginning of their new deployments. We’ll take a look at some examples below:

Premier Alliance

- PMR - EC3 has a blank sailing allotted to slot 5 and a TBN awaiting verification in slot 9. Despite the insertion of a strategic blank, the first several sailings, including the ONE EAGLE, ONE MANCHESTER, and ONE MANHATTAN are forecasted with -3 days delay or less. The first sailing, ONE EAGLE, currently has ETA 23-03-2025 into her first port of discharge at Halifax with 0 days delay.

- PMR - EC2 recently had one TBN in slot 4 revised as a blank sailing, and an additional TBN in slot 9 that persists for the time being. The first five sailings all start out with 0 days delay, with SEASPAN BENEFACTOR in slot 1 forecasted to make the first discharge call into Savannah on 21-03-2025.

Gemini Cooperation

- GEM - US1, a RTW service, had its proforma start dates pushed back from 02-02-2025 to 08-02-2025, confirmation arrived in the first week of January.

- GEM - US4 also had her proforma start dates pushed back at the start of January, from 04-02-2025 to 08-02-2025. This also necessitated a mass reordering of slot assignments, including former first sailing MADRID EXPRESS being pushed all the way to slot 14. The ROME EXPRESS will now commence the first sailing, with ETA into New York City 24-03-2025.

- GEM - US2, in contrast to its Gemini peers, this service had start dates pulled up by one week from 17-02-2025 to 10-02-2025 - changes confirmed as recently as mid-January. Additionally, not only do the first five sailings kick-off with a 0 day delay, but each of these vessels are transferring unique services like The Alliance’s EC2, PN2, PS6, and even non-alliance services like CMA’s EPIC2 or MEDEX services. The first sailing, MADRID EXPRESS, has a current ETA into New York of 22-03-2025.

Service examples: rotation comparisons

This is far from an exhaustive list of the interesting evolution of virgin services from their predecessors, and there’s no shortage of that on the East Coast with the prevalence of so many pendulum, RTW, and Cape bound routes.

We have highlighted a select few to once again illustrate the distribution of namesakes across the new alliances, and how altered port rotations, roundtrip lengths, vessel sizes, and other structural changes might be valued as potential contributors to improved reliability in 2025.

Premier Alliance

- THEA - EC1 transition to the PMR - EC1 will retain similarity as classic East Coast loops but the EC1 exhibits a reduced roundtrip of 77 days and a drop in 4 calls. Xiamen, both Manzanillo calls, and a call to Charleston are dropped but the rotation remains otherwise identical. There is also a shift in average vessel TEU from the 13K to 10K range and no carryover of specific vessel deployments from the EC1.

- THEA - EC5 evolution into the PMR - EC3 includes an increase of round trip time to 105 days and the addition of a single slot up to 15 total. The name difference may throw us for a loop here but the port rotation remains identical with the exception of Norfolk being bumped back to just after Charleston. A total of 5 ONE operated vessels will transfer over from the former EC5 for the first round of sailings, and one slot remains unverified at this time.

Gemini Cooperation

- 2M - ECNA Suez loop to GEM - US1, aka Maersk Line’s TP11, will become an RTW loop with the addition of an Eastbound call to the Panama Canal and the roundtrip will increase to 91 days up. In terms of port rotation there is little resemblance: Savannah will switch places with New York as the first and last load port along the East Coast and Charleston will be dropped for Norfolk. The Asian leg of the journey will look entirely different with the exception of a call to Singapore. Average vessel sizes remain in the 8 to 9K TEUs range but none of the predominantly Maersk vessel lineup from the 2M service end up deployed on the US1.

- 2M - ECNA RTW pendulum to GEM - US2, or Maersk Line’s TP12, was also mentioned in part one of our report because it becomes a 2 coast service. Calls to Yantian, Xiamen, Baltimore, Colombo, and the Cape of Good Hope are dropped for a reduction to an 84 day roundtrip. 2 calls into Cartagena are paired with the both Eastbound and Westbound Panama calls, and Los Angeles becomes the last North American load port. Average vessel sizes remain in the 10K TEUs range but there is no carryover of the former lineup whatsoever.

Non-Alliance

- MSC - Empire will carry over MSC’s name from the 2M - ECNA RTW pendulum but sees a reduced roundtrip of 77 days, down to 10 calls and 11 slots. Most notably, it becomes a classic East Coast loop route, dropping the Cape of Good Hope in favor of a second Panama call on its return to Asia. Yantian, Xiamen, Colombo, and Tanjung are dropped and a call to Qingdao is added. Average vessel TEU’s are closer to the 8K range as opposed to 2M’s 10K TEU vessels.

- MSC - Pelican which carries over its name from the 2M - US Gulf Panama loop, provides an opposing example. The MSC iteration of this service becomes a RTW route by dropping a Panama return call in favor of the Cape of Good Hope and an additional vessel slot for a total 84 day roundtrip. Cai Mep is dropped and Lazaro Cardenas is added. Miami is added as the new last load port out of the East Coast and joins sister Florida port, Tampa. Vessel lineups roughly align in the 9K TEUs and 5 ZIM vessels are directly carrying over their deployment from the 2M predecessor, there are still 3 slots with unverified TBN’s.

2M - US Gulf Panama loop vs. MSC - Pelican import rotation into Tampa, FL

2M - ECNA RTW pendulum vs. GEM - US2 import rotation into New York / New Jersey

Methodology notes

- Proforma events are planned calls that are based on service rotations provided by carrier fliers and long-term schedules. They are unique to each service version and measured as expected capacity.

- Actual events are calls that have already occurred and are reflected in our actual deployed capacity measurements. Some actual events do not have planned proforma schedules and are defined as inducements. Before an actual event has passed, it is classified as a forecasted event - distinct from proforma or expected capacity.

- Trade capacity and planned events on all counts in the analysis above were measured by the first port of discharge.

- When measuring trade capacity by trade, service, or alliance we prorate the values based on assumptions like 90% capacity being utilized at the last load port of the first leg of the journey. We also use this method to split the expected capacity for complex cargo flow services that call multiple regions in addition to the West Coast (ie Central America, East Coast North America).

- A last load port is the last call on the head haul of a cargo flow: on West Coast North America service rotations this will be defined by the final Asian port of call before the vessel sets out across the Pacific to North America. The first discharge port on the head haul is defined as the first port of call in the next leg of this cargo flow: that would be the first vessel’s first planned call in Canada or the United States.

Contact us: Please reach out to ops@eesea.com if you are an existing customer that would like to explore these stories in depth, contact@eesea.com if you are interested in collaborating on press releases or other third party publications, and commercial@eesea.com if you are a new user looking to test a use case and learn about what our data solutions can offer.

eeSea Signals

- Halifax Inbound/Outbound Calendar

- Montreal Inbound/Outbound Calendar

- New York/New Jersey Inbound/Outbound Calendar

- Savannah Inbound/Outbound Calendar

- Charleston Inbound/Outbound Calendar

- Norfolk / Virginia Inbound/Outbound Calendar

- Tampa Inbound/Outbound Calendar

- Miami Inbound/Outbound Calendar

- Houston Inbound/Outbound Calendar

- All Current + Upcoming Premier Alliance Services

- All Current + Upcoming Asia - North America Gemini Cooperation Services

- All Current + Upcoming Ocean Alliance Services

- eeSea TrueTransit Global Port Connectivity + Reliability Benchmarking for Far East - West Coast North America Trade

- Trade Lane Dashboard Including Schedule Reliability and Actual vs. Expected Capacity Timeline - Tableau Permission Required

- Port Calendar Including Vessel Forecasts + Delays by Service - Tableau Permission Required

- Trade Capacity Index Changes by Service + Port - Tableau Permission Required

- VSA Shares by Trade + Service - Tableau Permission Required

- Alliance Reshuffle Weekly Capacity Changes by Alliance - Tableau Permission Required