Mustang suspended

MSC revealed a major update to their Far East - West Coast North America schedules last week when they announced the suspension of the MSC - Mustang; the standalone service was set to make its first call into Long Beach this month. However, the sudden suspension may not have come as a complete shock to some as our own analysts were struggling to pin down details of vessel deployments right down to the wire.

While it was indicated in MSC’s announcement that the capacity would be taken elsewhere, the only vessel that had been determined in the lineup was the 16.6K TEU MSC AMSTERDAM. It’s unclear where she will now be redeployed and MSC’s own portal affirms there is no schedule information to be found currently for the ship.

European trades see-saw

That said, the Far East - Europe trade would be a likely candidate for her new deployment given the popular discussion in recent days that MSC would be redistributing capacity, including some larger ~19-24K TEU vessels, in favor of the Far East - Mediterranean and West Africa trades. If we examine the high-level impact of the current vessel lineup for the next 8 weeks on both standalone and Premier alliance services on the Far East - Europe subtrades, clearly favors Mediterranean ports.

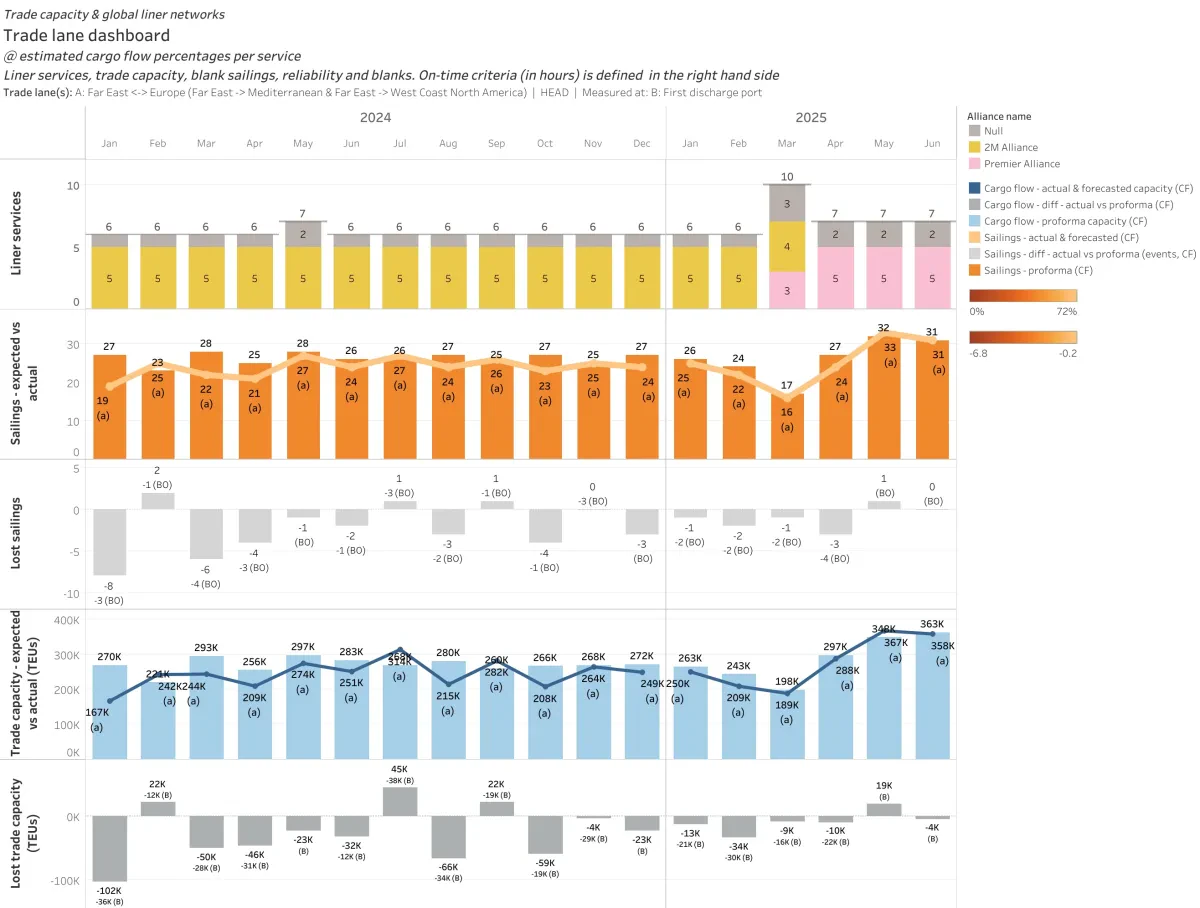

Monthly trade capacity - MSC in Far East - Mediterranean

Monthly trade capacity - MSC in Far East - Northern Europe

In Northern Europe, MSC’s expected (aka proforma) monthly capacity dips from an average of 432K TEU in the 6 months leading up to the network upheavals, down to 358K average monthly TEU in May and June: a decline of 17%. On the Mediterranean side, the 6 month average of 268K TEU through January 2025 rises to an average 356K TEUs in May and June: a 25% increase.

MSC’s capacity evolution strongly mirrors the larger trend towards increased capacity in the Far - East Mediterranean subtrade that we reported in our Far East - Europe trade review on February 17: The Far East - Mediterranean subtrade will see an increase in both alliance and non-alliance weekly capacity, at 1% and 18% increase respectively while Northern European ports decrease by 11% on alliance offerings and 15% in non-alliance service capacity.

Service details

For our readers that would appreciate a deeper understanding of which major services will witness an increase/decrease in average weekly capacity, we offer the following analysis of those that exhibit confirmed changes.

Far East - Mediterranean

- DECREASE: MSC - Phoenix (2M) @ 15K weekly TEU vs. MSC - Phoenix (standalone) @ 4.2K weekly TEU

- DECREASE: MSC - Jade (2M) @ 23.8K weekly TEU vs. MSC - Jade (standalone) @ 22.7K weekly TEU

- INCREASE: MSC - Dragon (standalone) @ 15.3K weekly TEU vs. MSC - Dragon (PMR) @ 16.3K weekly TEU

- INCREASE: No predecessor for MSC - Panther (PMR) @ 13.6K weekly TEU

Far East - Northern Europe

- DECREASE: MSC - Griffin (2M) @ 14.8K weekly TEU vs. MSC - Griffin (PMR) @ 10.8K TEU

- DECREASE: MSC - Albatros (2M) @ 18.9K weekly TEU vs. MSC - Albatros (standalone) @ 15.2K weekly TEU

- DECREASE: MSC - Lion (2M) @ 24K weekly TEU vs. MSC - Lion (PMR) @ 15.6K weekly TEU

- INCREASE: MSC - Silk (2M) @ 18.6K weekly TEU vs. MSC - Silk (PMR) @ 20.6K weekly TEU

- INCREASE: MSC - Condor (2M) @ 15.8 weekly TEU vs. MSC - Condor (PMR) @ 21.6K weekly TEU

For services where we currently expect a slow (or intermittent) transition towards larger vessels, upcoming vessel assignments still reflect a relatively stable average capacity but we will see increased weekly capacity as 90+ day schedules become more fixed. Notable examples here include the MSC - AFL and the MSC - New Falcon, two standalone serving the Far East - West Africa and Far East - Middle East trades respectively.

- MSC TIGER (PMR - MD3) will initially continue operating in the 18-19K TEU range. While the MSC ZOE (19.2K TEU) and MSC ANNA (19.4K TEU) will up the stakes in late March, the vessels that are currently following them in the lineup remain in the 16K TEU range.

- MSC - AFL will continue operating in the 16K TEU range despite the megamax additions of the MSC TESSA (24K TEU)and MSC GEMMA (24K TEU). Even though TESSA’s deployment begins this week, her nominal capacity will not be counted towards her first port of discharge in West Africa (Tema) until mid-April.

- MSC - New Falcon - Currently operating at an average 14K TEU weekly capacity will see vessels like the [MSC ERICA](MSC ERICA) (19.2K TEU), MSC MARIE (16K TEU), MSC TINA (19.2KTEU), phase in during this month. However, below average vessels like the MSC MARGRIT (12.2K TEU) and others in the 14K TEU range like MSC KALINA and MSC GENOVA mean the average weekly values remain stable for the foreseeable future.

Notes

- We define the pre-transition and transition period as October 28, 2024 - March 16, 2025 and March 17, 2025 - May 04, 2025; a total of 27 weeks/6 months:

- Please note the importance of interpreting average weekly capacity on a service level differently than how we factor aggregate monthly proforma capacity, which more accurately reflects the aggregate increase in capacity per individual vessel deployment.

eeSea Signals

- All Current + Upcoming MSC Services

- Trade Capacity Index (TCI) Evolution by Trade - Tableau Permission Required

- 2025 Weekly/Monthly Trade Capacity Evolution by Alliances - Tableau Permission Required

- VSA Shares by Trade + Service - Tableau Permission Required