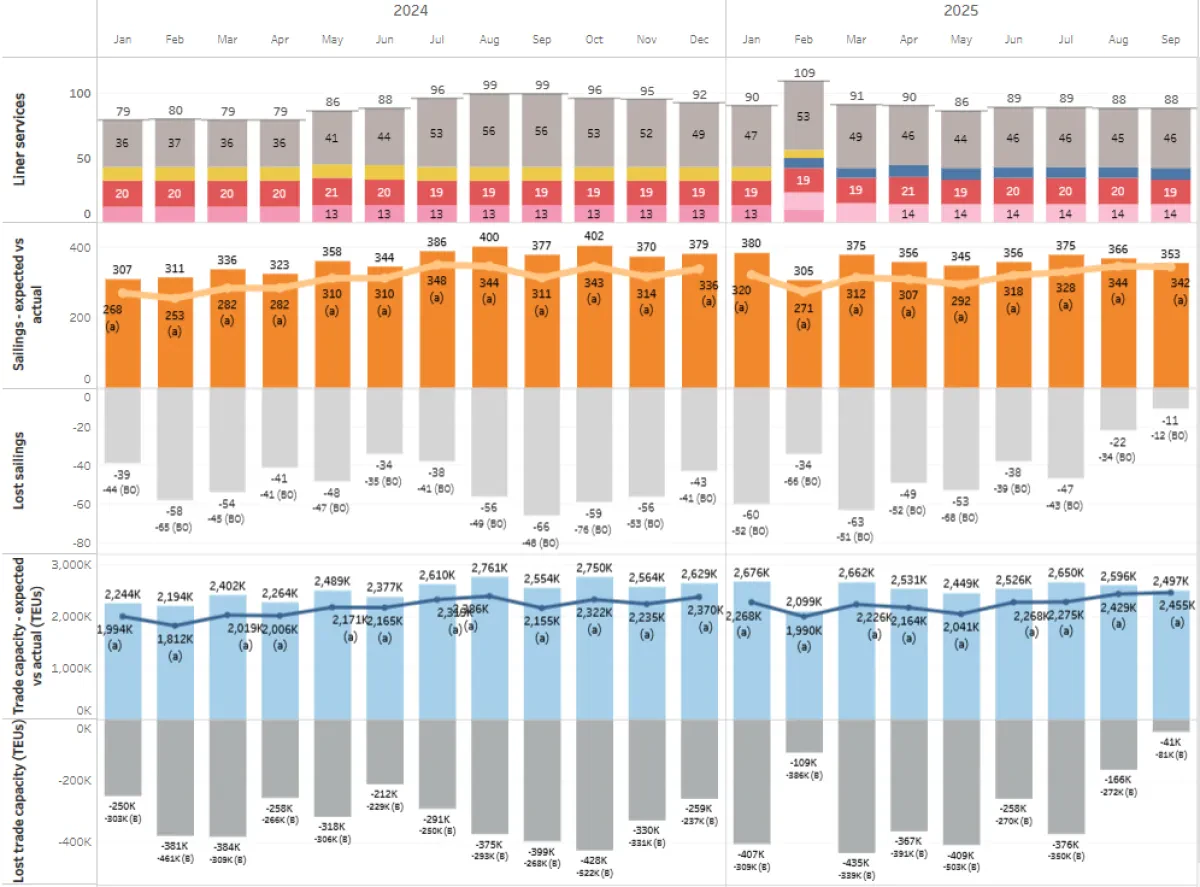

The ongoing tariff dispute between the United States and China has precipitated substantial disruptions throughout global maritime logistics, with North American trade routes experiencing particularly acute impacts. While carriers initially pursued a cautious wait-and-see approach, significant operational adjustments became evident across various service offerings as operators sought to maintain trade lane capacity equilibrium. The risk of overcapacity posed considerable financial exposure given the prevailing depressed freight rate environment, while cargo volumes contracted as shippers deferred shipment decisions pending more favorable market conditions. Consequently, major carriers and alliance partners implemented strategic capacity management initiatives, including blank sailing programs and comprehensive service restructuring, to address unprecedented market volatility.

However, these capacity reduction measures proved temporary as the industry now confronts an inverse market dynamic. The implementation of a 90-day tariff escalation moratorium has triggered an urgent cargo evacuation response from shippers, creating sudden demand surges that carriers must accommodate. This has resulted in renewed market instability within the shipping sector. eeSea's analysis confirms that carriers are now actively expanding capacity in anticipation of sustained demand growth. The following observations from our monitoring activities over the past week illustrate this strategic pivot:

Reversed Suspensions

1. ZIM - ZX2

The most significant service suspension was ZIM's ZX2 service. ZIM was among the initial carriers to withdraw from the transpacific trade in April. However, this suspension proved temporary, as the carrier has recently reinstated the service at full capacity without any blank sailings, indicating robust demand expectations. The suspended service represented approximately 18,000 TEUs of monthly capacity, and the reinstated iteration maintains identical capacity. The service continues to operate on a 35-day round trip schedule, consistent with its pre-suspension configuration. One notable development is ZIM’s full restoration of the service, with no foreseeable blank sailings in the near term. This move suggests a more optimistic outlook on demand from the carrier’s perspective.

2. MSC’s Orient and Empire Services

MSC appears to have undertaken the most significant service suspension measures in response to the recent tariff implementation. According to eeSea, the Swiss carrier temporarily suspended three transpacific services to the North American market. At their peak, these services represented a combined capacity of approximately 53,000 TEUs, based on measurements at the last-load port in March 2025.

Should demand continue to strengthen, MSC may reinstate this capacity. Notably, the MSC - Orient service has been partially restored, with five vessels scheduled beginning with the MSC TIANSHAN on July 23, 2025. However, the revised service includes two blank sailings, which may reflect ongoing market volatility and uncertainty around whether the 90-day tariff moratorium will be extended.

Further adjustments include the removal of Portland from the service rotation and an increase in berth stay at Long Beach from 5 to 7 days, potentially signaling MSC’s strategic intent to accommodate heightened activity or delays at this key U.S. port.

Similarly, MSC has reinstated its Empire service, which, like the Orient, was quietly suspended at the height of the tariff escalation. The restored service features several key changes, most notably the inclusion of Miami and Rodman in the port rotation. Despite these additions, the overall service roundtrip remains consistent with the pre-suspension version at 77 days. Out of the 11 scheduled vessel slots, MSC has currently deployed 9 vessels, with 2 blank sailings still in place, potentially indicating a cautious approach amid lingering market uncertainty. ZIM will continue its participation in the Empire service through a slot charter agreement.

MSC has also exhibited a series of uncertain adjustments, with the Sentosa service standing out as a particularly dynamic case, as noted by our analysts. Initially introduced as part of a pendulum service, Swan-Sentosa MSC quickly restructured the offering, splitting it into two distinct services: Swan serving the Asia - Europe trade, and Sentosa, focusing on North American ports.

Following this bifurcation, MSC began signaling a potential merger of the Clanga and Sentosa services, possibly aiming to re-establish a pendulum structure. However, this consolidation was ultimately not realized. Both Clanga and Sentosa continued to operate as independent services after the announcement of the tariff moratorium, reflecting the level of uncertainty that is currently surrounding the container shipping industry.

Restored Blank Sailings

Blank sailings have long been a strategic tool for carriers to swiftly address overcapacity and maintain trade lane capacity equilibrium and the recent tariff escalation was no exception. In response, carriers implemented a wave of blank sailings to mitigate the immediate impact on demand.

However, eeSea now confirms that carriers are actively reversing these blanks in light of improving market conditions. A notable example is the Ocean Alliance’s PSW1 service, which has reinstated all previously blanked sailings. Effectively, the service experienced a brief suspension period, during which all scheduled vessels were withdrawn. Full capacity is now restored, with operations resuming on May 31, 2025, marked by the CMA CGM Medea commencing the first post-suspension voyage.

The Ocean Alliance’s PSW5 service has similarly returned to full operational capacity, with only two blank sailings currently scheduled for August. CMA CGM’s Amerigo ervice has also reinstated two previously blanked sailings, further contributing to the trend of service normalization.

In addition, both the USEC2 and USEC3 services under the Ocean Alliance have each filled one blank sailing. The same applies to Ocean’s PNW1, PNW2, and PNW3 services, all of which have moved to reverse earlier capacity reductions. Collectively, these actions reflect a broader industry shift toward restoring network stability in anticipation of sustained demand recovery.

eeSea analysts anticipate that additional services will restore capacity as market conditions continue to stabilize. Given the prevailing uncertainty, the industry is likely to witness further reversals of blank sailings and the potential deployment of extra-loaders, as shippers seek to move as much cargo as possible during the moratorium window.

We will continue to monitor these developments closely and provide timely updates as the situation evolves.