Regional carriers, along with CMA & COSCO, have gained steady confidence in operating small to medium sized vessel strings through the Houthi controlled Bab-el-Mandeb strait over the past 12 months. While the Asia - Europe trade has largely suffered from longer transit times and increased CO2 emissions tied to military conflict in the zone, the secondary Asia - Middle East trade serving the Red Sea is finally witnessing a quiet revival.

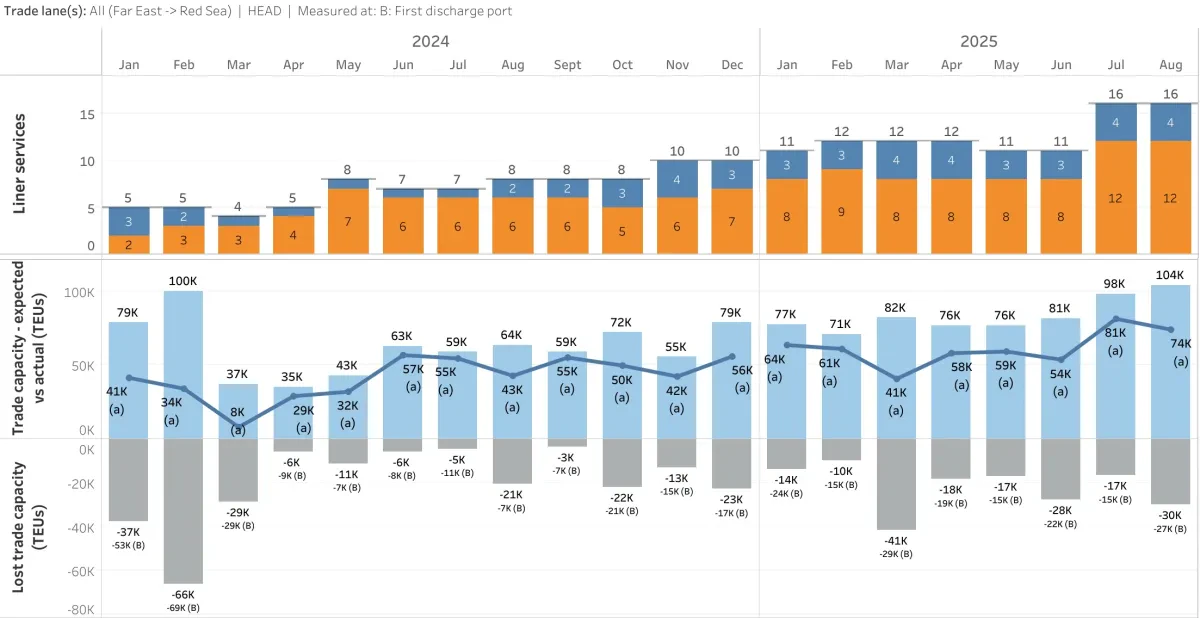

Asia - Red Sea Expected vs. Actual Trade Capacity Timeline

The number of unique service versions on this trade has doubled since Q3 2024, when there was an average of 8 services any given month. This gradual comeback now boasts 16 services and a 54% YTD planned capacity increase that is set to peak at 104K TEU of proforma capacity in August.

A score of new or improved services announced as recently as Q2 2025 are not restricted to regional carriers alone and include the following highlights:

- The REX - X, a China United Lines future extraloader service complementing the CUL - REX that commenced in December 2023. Commences the final week of August.

- COSCO increased the frequency of the RES2, operated alongside PIL since March 2024, up from a 12 day to a weekly service with the addition of three more sailings at the end of April.

- COSCO also introduced an additional RES1 service in early May, partnering with OOCL and currently operating with just three general cargo vessels.

- Kawa Shipping’s EMX1 which commenced in March has increased from a 21 day to 7 day frequency in June with the addition of 4 more vessels.

- Wan Hai Lines will likewise be doubling the number of vessels on their AR2 service up to 8 later this month, increasing the frequency from 14 to 7 days.

- Sea Legend Shipping, an India based carrier, introduced their Asia - Red Sea service in mid-June but only 3 of 9 available slots are currently providing voyages.

- CStar Lines announced the commencement of FRS1, FRS1 - X, and the FRS2 in May and June.

- SeaLead Shipping recently reinstated their CRS service, which had not been operational since December 2022.

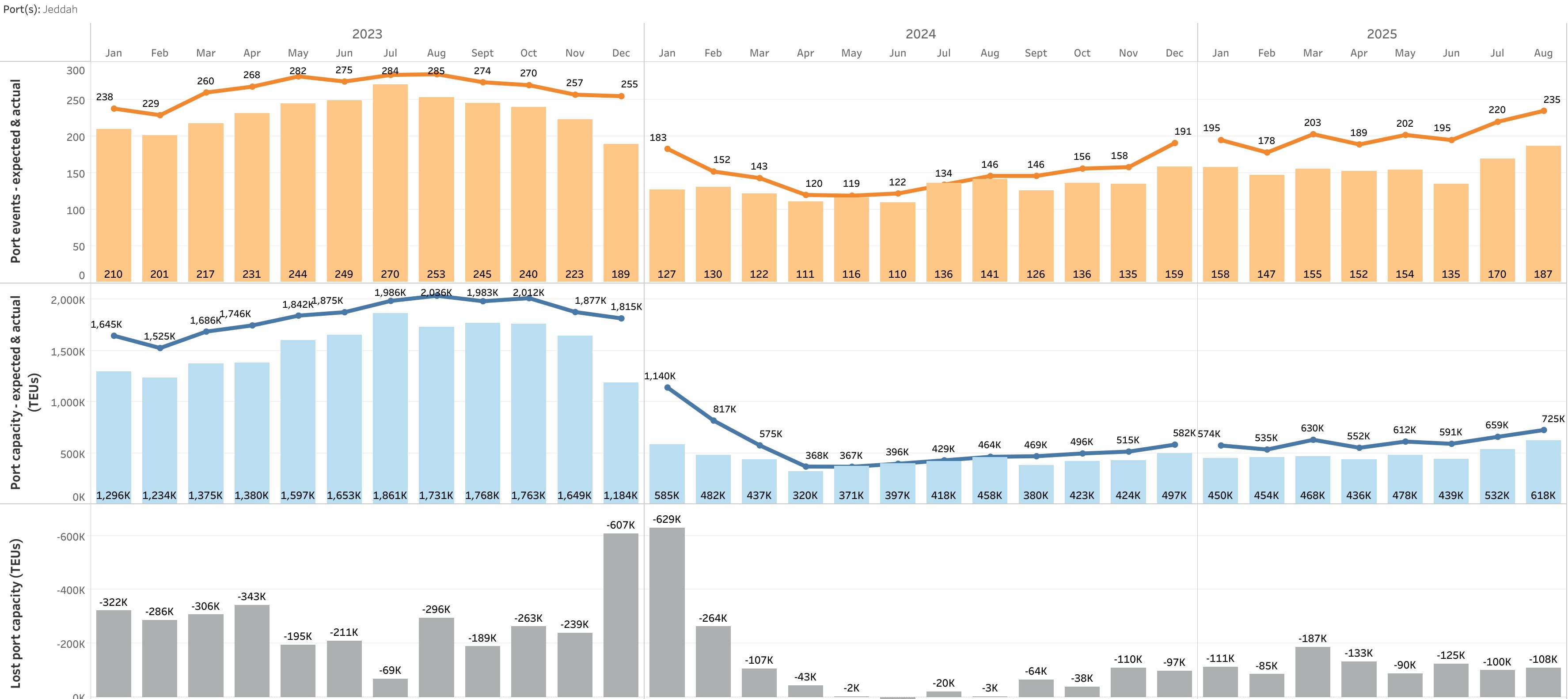

Jeddah Expected vs. Actual Trade Capacity Timeline

The resurgence of Red Sea capacity from Asia is echoed - albeit a bit more modestly - at the port of Jeddah, which serves as the primary port of discharge for the subtrade services. Jeddah saw average actual monthly capacity across all trades slide by an astounding 72% after Houthi involvement in the Israel-Gaza war began in November 2023. The port, which hosted an average 1.65 Million TEU of actual monthly capacity in 2023, plummeted to 432K in 2024 and has since seen a slight uptick to 466K of actual capacity arriving every month in 2025.

There are currently 18 Asia - Europe services that continue to operate through the Bab-el-Mandeb strait and the Suez Canal, with 39% of these calling ports outside the East Mediterranean and 33% making direct calls to Russian ports. An additional 2 strings calling Jeddah on their way to the Suez Canal were introduced as recently as April by CSTAR, the FEM1 and IMB1. While this cargo flow contributes less capacity to Jeddah than uniquely Red Sea bound services, it's remarkable that all container vessels routinely traversing these dangerous waters on a major E/W trade - excepting Ocean Alliance's MED5 - are operated by smaller regional carriers.

eeSea Signals

- All Asia - Red Sea Services

- All Asia - Europe Services Utilizing Suez Canal

- Port Pair Options + Schedule Reliability Between Asia - Jeddah

- Trade Capacity Index (TCI) + Schedule Reliability Evolution for Asia - Red Sea - Tableau Permission Required

- Trade Capacity Index (TCI) + Schedule Reliability Evolution for Jeddah - Tableau Permission Required

- Asia - Red Sea Services by VSA, Avg. TEU, etc. - Tableau Permission Required

All capacity values are measured at first discharge port for the purposes of this analysis.