Average spot rates increased in October on major fronthaul trades from Far East to Europe and US, bucking the general downward trend in recent months – how do shippers make sense of this spike when many are preparing to tender for new contracts?

The October uptick could set alarm bells ringing for shippers hoping for a less painful 2026 - market sentiment is a powerful force – but they would be well served to remain calm and use data to gain a more balanced view of the situation.

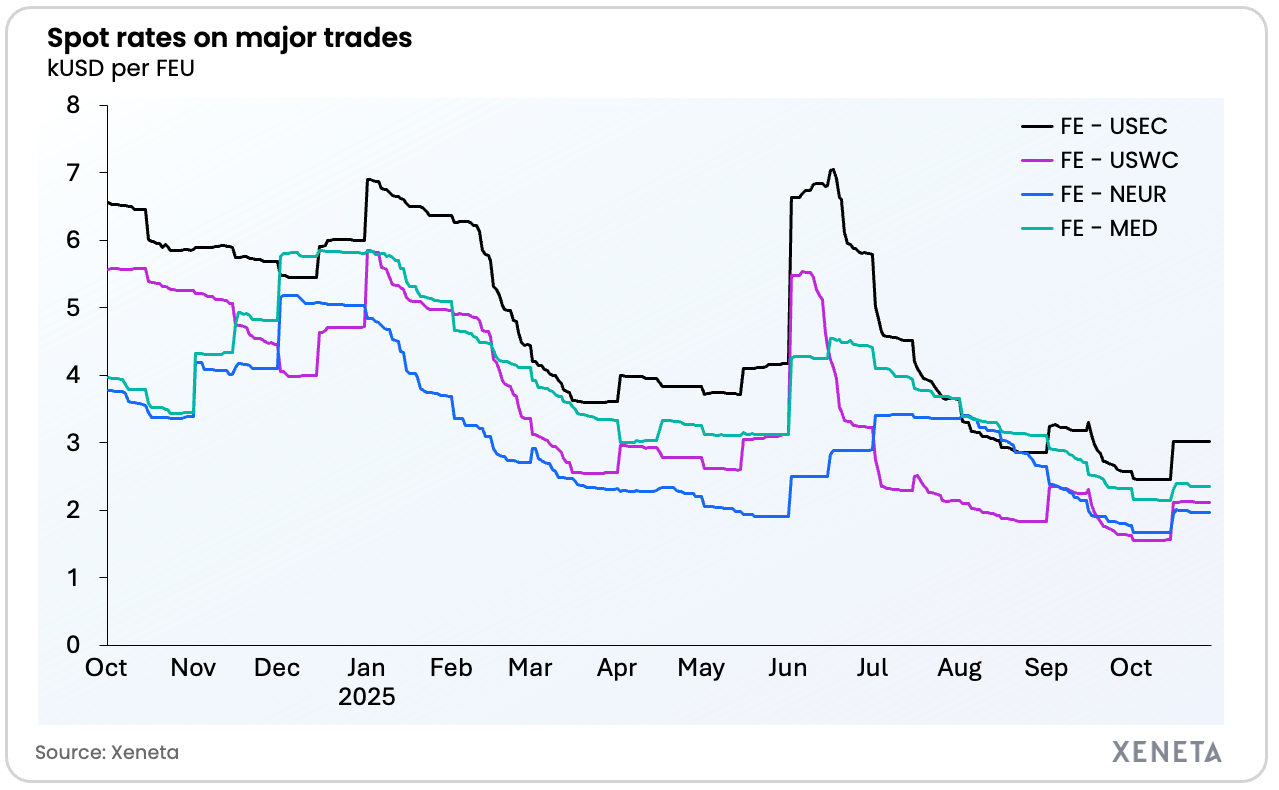

Where do rates stand? Average spot rates from Far East to US West Coast and US East Coast are up 38% and 23% compared to 1 October at USD 2138 per FEU (40ft container) and USD 3038 per FEU respectively.

Into North Europe and Mediterranean, average spot rates are up 18% and 9% in the same period to stand at USD 1968 per FEU and 2338per FEU.

On both Transpacific and into Europe, early data suggests spot rates will rise again at the start of November.

{kind=link}

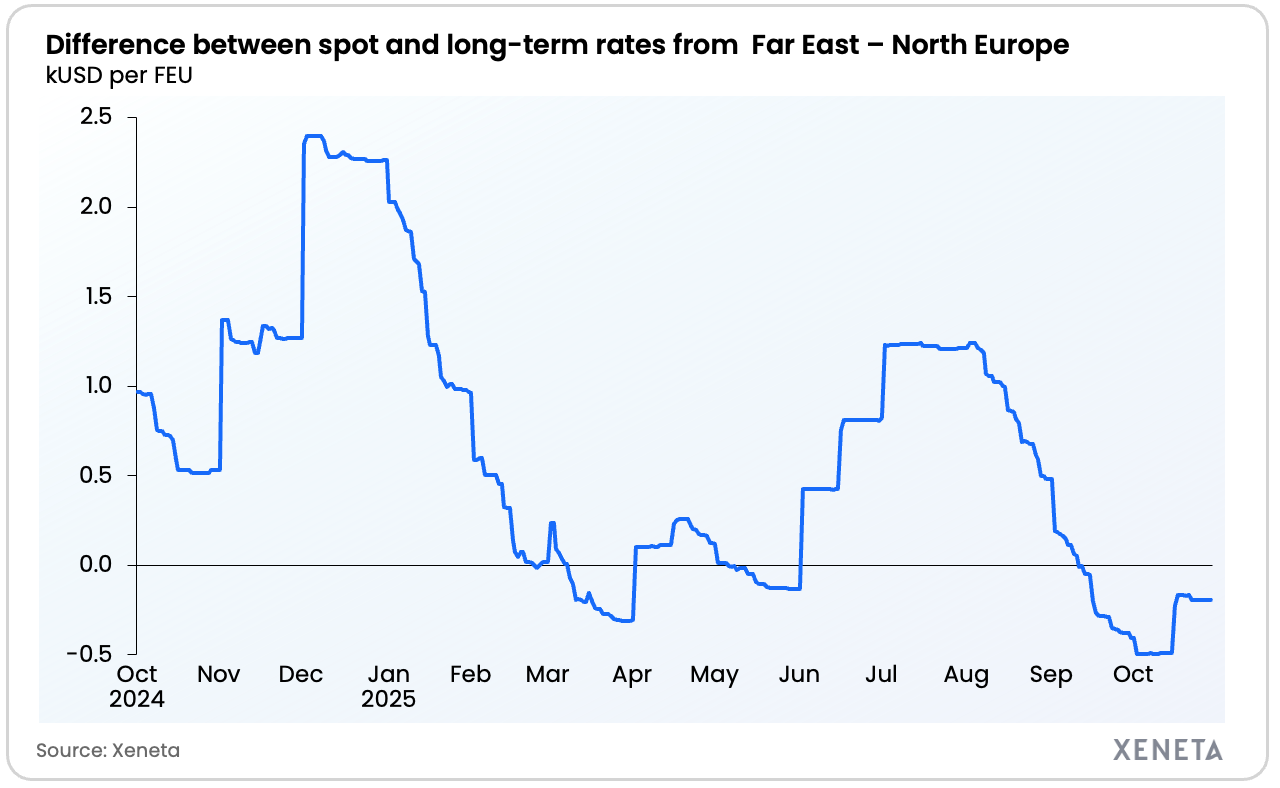

Spot rates compared to long term contract rates

Critical for shippers heading into tender negotiations is the spread between the spot market and long term market (contracts signed in past three months).

Looking at Far East to North Europe, even after the mid-October increase, average spot rates still sit USD 200 per FEU below the average long term rate. Even if spot rates rise further as expected on 1 November, it may only bring parity with long term rates, meaning shippers will still be in a strong position when negotiating new contracts.

{kind=link}

Put simply, why would a shipper lock into long term rates that are higher than short term rates?

On the Transpacific trade to US West Coast, the mid-October spike brought spot rates back above the average long term rates – but the spread is only USD 125 per FEU.

Why are spot rates increasing? The spot rate increase into the US can be partly explained by carriers having removed too much capacity compared to demand – October saw the lowest deployed capacity on the trade into the US West Coast since the aftermath of Liberation Day on 1 April when demand fell dramatically due to Trump’s sweeping tariffs.

There is also an argument that it is no coincidence spot rates increase just at the time of year when shippers are gearing up for tenders. Carriers know the importance of market sentiment and do not want to negotiate at a time of falling rates – they will be working as hard as possible to make sure that isn’t the case.

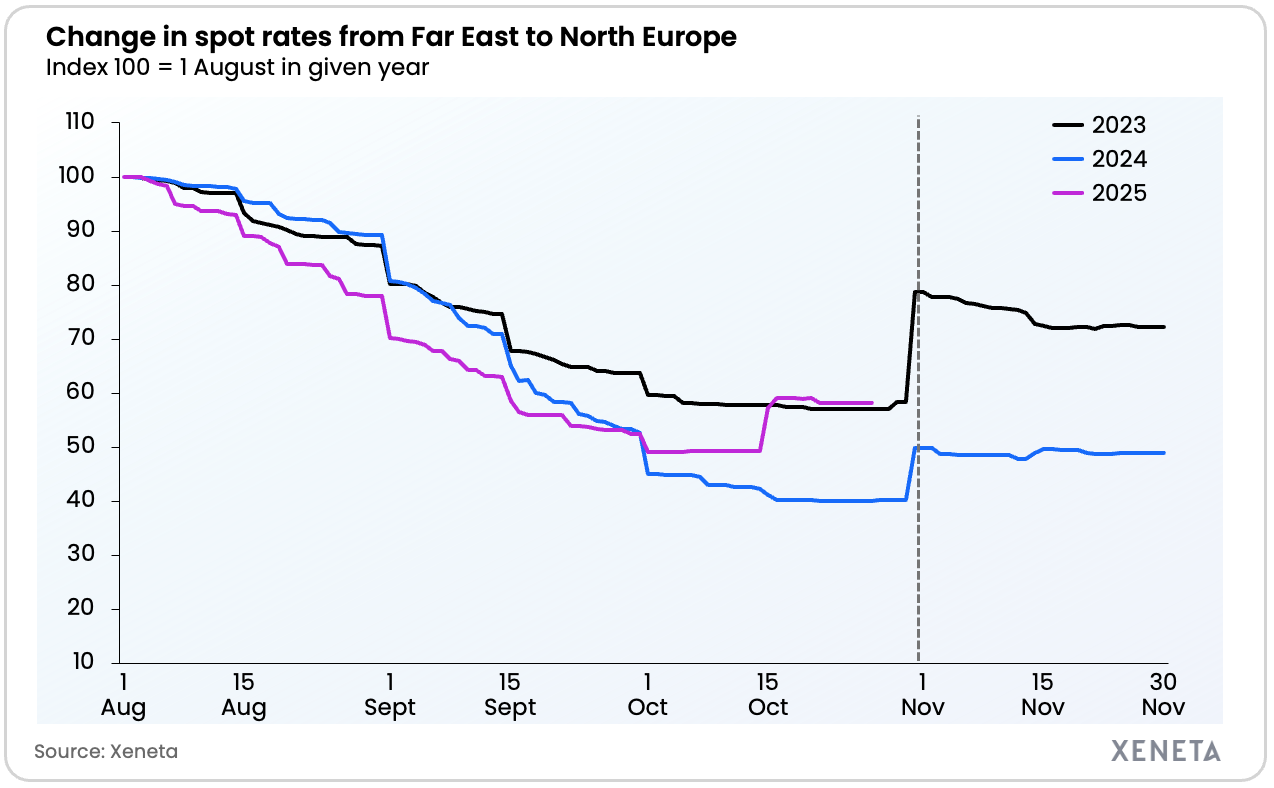

In the past two years, average spot rates from the Far East to North Europe have increased on 1 November following months of decline.

This could be a coincidence, but the case for it being a result of timely and effective capacity management by carriers is strengthened in the fact the rate increases come at a time when volumes traditionally fall during October and November.

{kind=link}

The spot rate increases have come a little earlier this year in mid-October, and there will be other factors contributing to the spike in addition to carrier capacity management, but the pattern is clear.

How should shippers respond?

The Xeneta Ocean Outlook 2026 was published this month and sets out expectations for overall lower long term and short term rates next year as overcapacity continues to plague carriers.

This forecast remains solid despite the latest rises in spot rates.

Average spot rates from Far East to North Europe are down 41% compared to one year ago, while long term rates are down 24%. From Far East to US West Coast, average spot rates are down 60% and long term rates are down 42%.

Shippers are going to be looking at securing better contract rates for 2026 than they were when negotiating 2025 rates.

Longer term expectations also impact long term rates

There is plenty for shippers to learn by looking back to 2025 contract negotiations.

An important takeaway from 12 months ago is that spot rates rising in Q4 does not necessarily translate into higher long term rates for contracts starting on 1 January.

Long term rates entering validity in January 2025 came in at the same level as long term rates in Q4 2024.

Shippers can also get a steer on carrier tactics for the upcoming tender season by looking back 12 months.

Analysis carried out by Xeneta earlier this year for a customer-exclusive tender report showed shippers entering new contracts on 1 January secured significantly lower rates if signing up for longer agreements.

Carriers were incentivizing shippers to enter longer contracts because rates were expected to continue to decline during 2025 against a backdrop of overcapacity.

Note: 12 months ago there was the known risk of Trump’s tariff policy, but few could have predicted the scale of what was to come.

From the Far East to Mediterranean, contracts lasting more than six months (vast majority of these were annual contracts) had rates 45% lower than contracts lasting three to six months. Smaller, but still substantial discounts could also be found on other trades.

Opportunities for shippers

Short-term dynamics on the spot market can, of course, not be ignored - but neither should full-year expectations.

The overcapacity carriers will need to overcome in 2026 should not be forgotten purely because they have successfully managed to push short term rates up at this point in time.

With the global container shipping fleet expected to increase 3.6% in 2026 (measured in TEU) against an increase in container shipping demand of 3%, the overcapacity headache is only going to get worse for carriers.

Carriers will be fighting hard for volumes to fill these vessels and will be incentivizing shippers once again – whether that is lower rates for longer contracts or the promise of better reliability performance.

2026 will be another challenging year for shippers, but there are plenty of opportunities to seize in their new contracts.

Source: Xeneta