Highlights

- Global OTP slightly improved to 30%

- Gemini remains the no 1 alliance, but is on a downward slide

- Hapag-Lloyd jumps to second in the carrier ranking, while Maersk remains no 1

- Far East - Europe head haul trade reliability drops from 40% in March to 28% in April

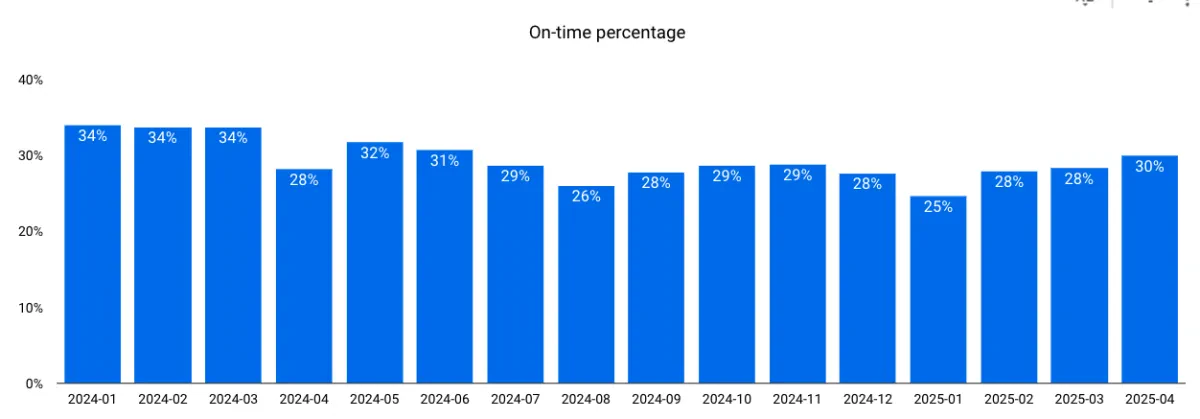

Global reliability on an upward trajectory

Two days into May, and eeSea is ready to bring you the April numbers from our Schedule Reliability Scorecard (SRS).

Global reliability lands at 30% OTP, only a very slight improvement on the previous months but nonetheless a continued one since January (25%).

The on-time percentage would, however, still need a big nudge upwards in order to reach the pre-pandemic high of 72% seen in May 2020.

Gemini Cooperation still in secure 1st place

Gemini drops from 87% for Q1 2025 to 82% in April 2025, but remains the indisputable no 1. In joint second place are Ocean and Premier, both at 25%. Non-alliance carriers total at 30% in April 2025. MSC outside Premier Alliance remains at 22% in April compared to 22% in March, 28% in Feb and 19% in Jan 2025.

Gemini, however, seem to be losing steam in the quest for 90%. They were stabilizing around 83% over the past 4 weeks, but dropped to their lowest full week at 79% in week 17. Considering the roll-out of the alliances, Gemini clocked 287 port calls in week 17 - and once the network is fully phased in we expect 310+ calls per week. Hapag-Lloyd continues to lead within the Gemini, with an 88% YTD performance vs Maersk's 82%.

THEA and 2M are on their very last calls.

Maersk still indisputable no 1 ocean carrier

Maersk remains the in first place when it comes to carrier reliability measured by vessel operator; they continue the upward trajectory seen since January 2025 (37% OTP) and make a remarkable rise through Feb 2025 (47% OTP) and March 2025 (52% OTP) to 57% in April 25.

With only a few decimals separating second and third place, Hapag-Lloyd takes second with a 42.8% OTP, followed by Wan Hai on 42.1%.

Hapag-Lloyd has taken a major jump compared to both Q1-25 and Q4-24 where the OTP was at 26% and 29% respectively. Wan Hai has also made a remarkable recovery, increasing their OTP by 19%-point since Q1-25.

This changes the scenery radically from Q1 2025 when Zim was in second and Cosco in third. Zim has dropped to 4th place, Cosco to 5th.

Measuring by VSA partner, Maersk, Hapag-Lloyd and Wan Hai also make up the top three, and the same trajectory as described above.

Significant drop on Far East - Europe trade

The Far East - Europe westbound trade exhibits a significant drop in OTP, with April ending at 28% OTP compared to 40% in March. This is amongst others related to the congestion delays in Northern European ports.

Far East - North America eastbound stabilizes at 37% OTP in April, similar to the numbers in March and Feb. These three months are still the best performance since Jan 2024.

Africa services decreased significantly since January (36% OTP), losing 13%-point in April. The same goes for South America East Coast services which is on a downward trajectory since January 25 (32% OTP), ending up at 18% in April.

South America West Coast is back as the best performing trade (43% OTP in April), primarily because of the reefer exports. Oceania, Middle East and Europe - North America services round out the global trade lane rankings at 23%, 29% and 35% OTP respectively.